One of the many benefits of writing a blog is the challenge of organizing your thoughts and having them questioned. It’s initially scary to put it out there, but as time passes there is a subtle switch from scary to educational. Our interactions have developed into a mutually beneficial relationship of learning. We rarely all agree on financial topics like the efficient market, behavioral finance, and saving till you are blue in the face. However, your rebuttals, comments, and suggestions expand and test my own understanding, which in turn creates better articles and mailbags. So, without further ado, our latest mailbag on CAPE ratio, bridge loans and hard money.

The Mailbag: CAPE Ratio

You mention CAPE a lot and it doesn’t seem to be what Superman wears, care to explain?

I refer to CAPE a lot when discussing market cycles and long-term returns. I believe it is one of the better data points used to gauge market valuation, particularly when there is a lot of movement due to forces other than value.

CAPE is a market valuation metric that is also referred to as P/E 10 or Shiller PE. It stands for Cyclically Adjusted Price to Earnings and is expressed as a ratio. The ratio averages a business’s or market’s inflation-adjusted earnings over a predetermined time period, most commonly 10 years. The inflation-adjusted earnings are then compared to the price of the business or market. The concept is that adjusting for inflation smooths out otherwise erratic swings in earnings, which makes it easier to see how healthy the business or market really is.

CAPE stands out from other ratios because it has a track record of successfully predicting long-term market returns, is based on business fundamentals and can be tied to human behavioral biases. Robert Shiller popularized the ratio in 1998 when he published a paper with John Campbell that concluded the market was overvalued and would be 40% lower in the next 10 years. The 2008 market crash that saw a 60 percent decline occurred exactly 10 years later.

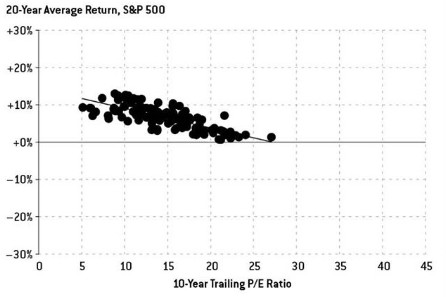

CAPE is one of the first metrics to successfully challenge efficient market theory with empirical data. We here at HIT Investments use it as one of our long-term investing guides. The data shows why. Check out this chart from Nate Silver, author of “The Signal and the Noise: Why So Many Predictions Fail — But Some Don’t.”

The chart shows that over a ten-year period, a higher CAPE means lower average 20-year returns. The result makes practical sense as well. If you pay more for an investment, it should take longer to pay off.

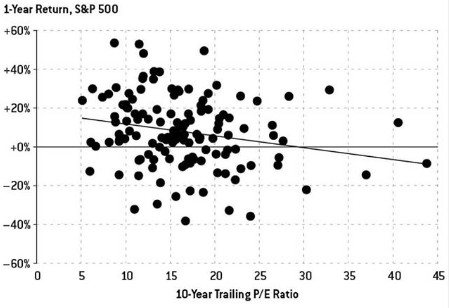

CAPE is one of the more popular ratios within the academic community and is not without controversy. Some believe that instead of being a signal, it is market noise that should be ignored. Over a short time span, that is true. Check out Nate’s chart below on the CAPE’s short-term return prediction capacity. The plot looks like an erratic machine gun spray.

Luckily for us, this machine gun spray over the short-term camouflages CAPE’s otherwise valid long-term signal and allows us to keep the advantage to ourselves. We accept the ineffectiveness of using CAPE ratio over the short term and acknowledge we cannot use this as a market timing mechanism. However, that’s no reason to ignore the data that proves it is an effective long-term evaluation tool.

If you want to look under the hood from time to time as well, my favorite site to check out the S&P 500’s current CAPE is here.

Hard Money & Bridge Loans

When looking into P2P real estate I encountered bridge and hard money loans. Could you expand upon what they are?

Bridge and hard money loans make up the majority of real estate loans found on peer to peer marketplaces. They are generally short-term loans with relatively high interest rates that are backed by collateral. Hard money and bridge loans skirt the traditional mortgage process and have the benefit of being fast and flexible to the borrower.

A hard money loan is a short-term mortgage. A home purchaser could submit a “cash offer” to the seller, but in reality, they plan to use hard money and not the cash in their checking account.

A bridge loan is short-term interim financing. A cash poor home buyer needs a bridge loan if there is a lag in selling their old home after agreeing to purchase a new one. The bridge loan is secured against equity in their old home and gives them the cash needed for their new home. Bridge loans are available for those who are asset rich and cash poor.

Bridge and hard money real estate loans have been thrust into the spotlight as they recently became available to invest in through Peer to Peer marketplaces. Many risks are still unknown because data is scarce, and the markets are relatively new, but in our latest article on fixed income, they were ranked #1 in terms of estimated returns. They are something to keep an eye on and a potential investment vehicle for those that can handle high risk and uncertainty for the prospect of above-average fixed income returns.