Loss aversion refers to our tendency to strongly prefer avoiding losses over acquiring gains. This behavior is at work when we make choices that include both the possibility of a loss or gain. For example, when making investment decisions we most often focus on the risks associated with the investment rather than the potential gains.

The loss aversion bias is not always dreadful to have, as in many cases it is beneficial to our way of life. Naturally responding more powerfully to threats than to opportunities is a clear example of our innate survival instinct. A benefit of loss aversion within the financial realm is its ability to help us shy away from investments that are potentially ruinous to our financial health and lifestyle.

Behavioral science experts Amos Tversky and Daniel Kahneman performed an experiment which resulted in a clear example of human bias towards losses. The experiment involved asking people if they would accept a bet based on the flip of a coin. If the coin came up tails the person would lose $100, and if it came up heads they would win $200. The results of the experiment showed that on average people needed to gain about twice (1.5x – 2.5x) as much as they were willing to lose in order to proceed forward with the bet (meaning the potential gain must have been at least twice as much as the potential loss).

If we are not aware and do not account for the bias towards loss it can push us away from rationality and when we invest it is of utmost importance for us to work towards rational and reasonable behavior.

Loss aversion derives from our innate motive to prefer avoiding losses rather than achieving similar gains. Knowing that this bias exists and how it affects our decision making is our ultimate goal. We cannot eliminate loss aversion, but we can be aware of it. Let our awareness not only prevent us from making irrational decisions but also help us to achieve more. See how the following examples of loss aversion can be a detriment or benefit to you:

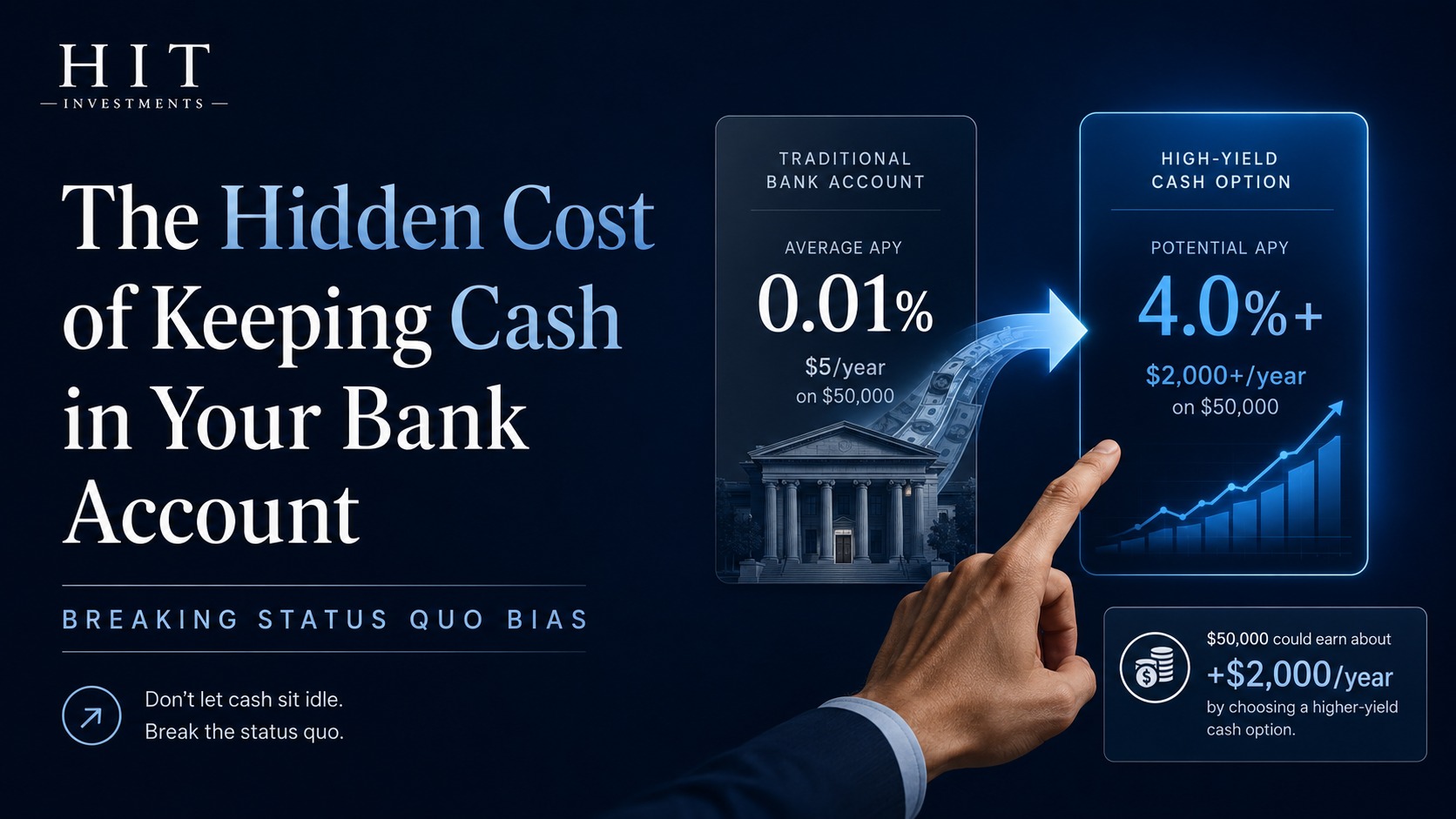

1. Investing solely in safe products that have little to no interest and as time passes inflation reduces/eliminates your purchasing power.

2. Not selling a stock that is below the price you paid strictly because you do not want to take a loss.

3. Selling a stock because it is greater than the price you paid just to lock in the profits.

4. Not accepting a deal below your baseline, not because the deal was poor, but because you could not bear the concession.

5. Inability to agree to a new contract due to having to make concessions in reference to an obsolete contract, even if the new deal benefits both sides.

6. The unwillingness to sell your house for less money than you paid for it.

7. Working harder and accomplishing more in an attempt to achieve a stretch goal.

8. Relaxing and slacking off after achieving an easy goal.

9. Not willing to change or press the status quo.

10. Visiting your financial advisor with a goal of building wealth and walking out with a life insurance policy.

11. Focusing on one investment that has lost money while ignoring the other investments.

12. Selling winning investments instead of losing investments for the sole reason of not accepting defeat.

13. Believing you haven’t lost until you sell.

14. Selling to avoid further losses when the reasoning for the investment says to buy more.

15. An inability to distinguish between a poor outcome and a bad decision when feeling regret after taking a loss.

16. Profit taking, selling an investment that has appreciated because you are afraid the profit may go away.

Did you find the example that was a benefit?

References

Peter Sokol-Hessner et al., “Thinking Like a Trader Selectively Reduces Individuals’ Loss Aversion,”

Thinking, Fast and Slow by Daniel Kahneman

Nathan Novemsky and Daniel Kahneman, “The Boundaries of Loss Aversion,” Journal of Marketing Research 42

www.behavioraleconomics.com