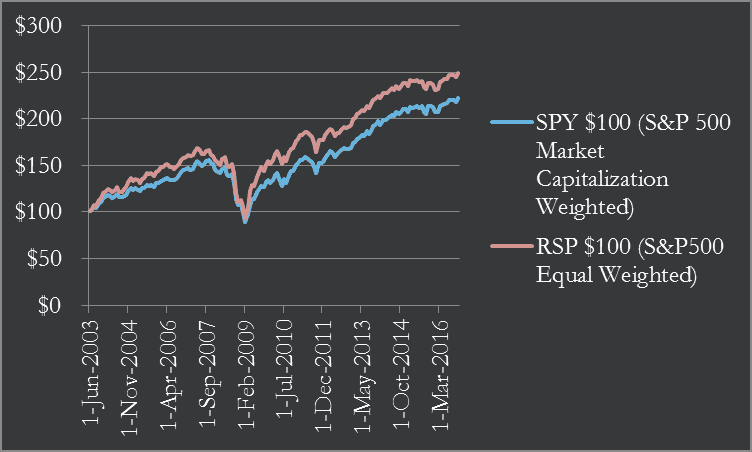

Data for SPY & RSP sourced from Yahoo Finance. Chart displays growth of $100 beginning 6/1/2003 through 11/1/2016

Then, if you take your diversification further by trying to invest in literally everything you come across (true diversification) you open yourself up to being taken advantage of through inefficient investment products. (You no longer have a handle on what you’re investing in because you’re spread too thin).

So if you want to outperform but don’t want to become a victim, should you still diversify? Yes, but in moderation. Diversifying moderately allows you to make mistakes without the consequences of having to start completely over, and being human, mistakes are inevitable. (A personal example is investing in the bank Wachovia before the financial crisis, ouch!).

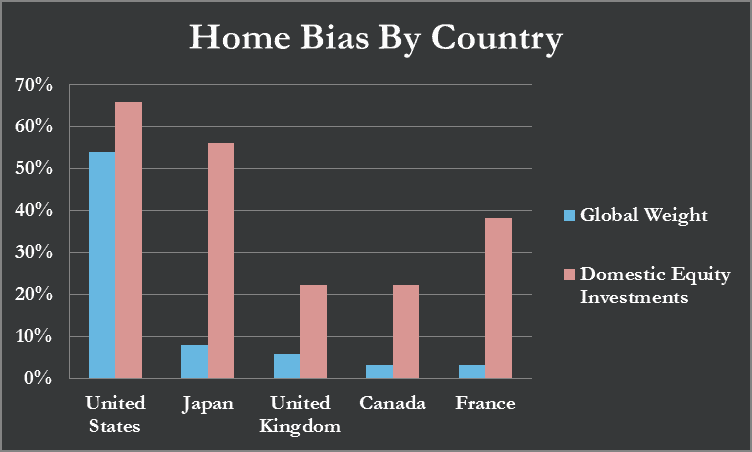

In conclusion, when you reflect on your personal portfolio, are you moderately diversified for the right reasons? Are your allocations home biased because of personal expertise, a tilt towards value, or an ability to minimize costs? Is your home bias driven by personal or moral reasons, maybe patriotism, community pride, or an inheritance? Or are you diversified for the wrong reasons: availability bias, overconfidence, herd mentality, or even an illusion of control.

If you find your portfolio allocations are diversified for the wrong reasons maybe it is time to think about updating your allocation strategy.

References:

International Monetary Fund

MSCI All World Index

Home Bias in International Equity Portfolios: a Review Piet Sercu and Rosanne Vanp´ee

Home Bias Re-Visited, Geert Bekaert and Xiaozheng Wang, Columbia Business School

The buck stops here: The global case for strategic asset allocation and an examination of home bias Vanguard – July 2016